Companies in the Facility Services sector — such as janitorial, HVAC, alarm security, fire protection and window washing companies, among others — represent a highly attractive target for private equity (PE) investors for several reasons. These companies usually have recurring revenue streams with long contract terms and contracts that renew automatically. Some services also provide a relatively recession-resistant investment since they are considered essential or mandated services for compliance and other reasons.

The sector is a highly fragmented one, with businesses that offer a wide range of services providing easy consolidation opportunities for investors with an eye toward gaining market share geographically. Combining different services under one roof can expand business as customers prefer one point of contact for all their outsourced service needs.

Investors can see the opportunities to drive value through economies of scale, especially by offering volume-based vendor discounts.

The size of the Facilities Services industry, which includes both soft services like janitorial work as well as hard services like HVAC and fire safety, is estimated to be $1.33 trillion in 2024 and reach $1.66 trillion by 2029, indicating a compound annual growth rate of about 4.66 percent.1

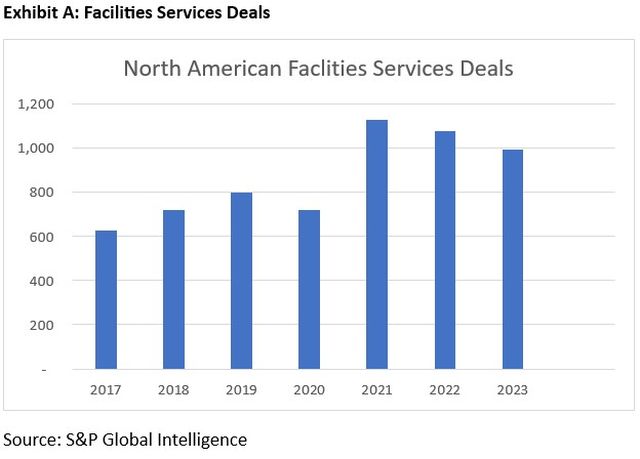

Transactions across the industry have been trending upward over the past several years, reflecting the attractiveness of value-driven opportunities and growth through roll ups and synergies to PE firms.

Growth in Facilities Services Dealmaking

PE investors are finding they can infuse further value into consolidated businesses by employing technology to predict maintenance demand, monitor energy consumption, track assets and optimize other areas of the portfolio company. Small improvements in technology can significantly enhance the overall delivery and performance of the business, especially as some PEs expand their investments from commercial to residential services.

Finally, the ability to buy and grow the business in a short window of time, depending on the level of integration, can make a big difference when it's time to consider exiting the business.

The Three Main Areas to Evaluate a Deal in This Sector

While PE investors must consider many factors when conducting due diligence, these three areas can indicate the attractiveness of the acquisition target and highlight the best opportunities to drive value after a deal is completed.

Financial

- Customer wins versus losses run rate: Evaluate the stickiness of customer relationships. The characterization of the typical Facilities Services business is a recurring and automatically renewing revenue base, so significant wins or losses in customer retention during recent periods can result in meaningful differences between historical and future earnings. Run-rate considerations for material wins and losses should be weighed when assessing the value of the business.

- Margin analysis: Differences in how a business classifies certain costs can drive wide disparities in how gross margin is evaluated or compared to peers. For example, whether a business locates supervisory managers within the cost of sales or under operating expenses can impact gross margin. When adding on a target to an existing portfolio company, buyers should ensure that a detailed analysis of the cost structure and the classification of those costs is performed so that there are no surprises in gross margin pre- versus post-acquisition.

- Revenue recognition: In services businesses where revenue is recognized over time based on percentage of completion, a full historic analysis should be performed using cost-to-cost comparisons, expended efforts evaluations or units-of-delivery methodology. Depending on the level of accuracy in management's estimation methods, there could be material differences in revenue recognized.

- Risks of poor financial controls and quality of information: Smaller, founder-owned businesses tend to be less sophisticated and have looser financial controls in place. In order to fully understand the target's cash inflows and outflows, a cash proof or reconciliation exercise is typically called for during the due diligence process. Focus a higher level of scrutiny around the balance sheet to confirm proper recognition and reconciliation.

Human Resources

- Employee retention: Within the industry, certain sub-sector populations such as janitorial services have turnover rates of more than 100 percent. Workers are often performing second shift work with limited ability for measurement or recognition. Buyers should ensure that the business can sustain its current headcount and growth trajectory without incurring material additional costs.

- Unionization: Building services, janitorial work, security services and other sub-sector industries are commonly unionized outside of right-to-work states. Union populations are often party to union-sponsored benefit plans, which can be more generous than non-union programs or multiemployer pension plans (MEPs.) MEP participation carries the risk of significant financial burden due to withdrawal liabilities in the case of a union exit. Buyers should quantify these contingent risks and determine any impact on overall valuation.

- Employment classification: Facility service employees are commonly operating at the direction of their employer, utilizing company equipment and uniforms. In situations where employees are misclassified as contractors and source their own teams for staffing, compliance issues can arise.

- Wage and Hour laws: Employers with large hourly populations can often run afoul of complex and changing wage and hour laws when expanding into new states. These can include overtime or spread hours rules, meal and wage breaks and changes to minimum wages. We recommend an investor complete a comprehensive diligence exercise to ensure no past risks or high costs to correct procedures.

Tax

- Sales Tax: States have disparate treatment regarding the taxability of different facility and environmental services. For smaller targets, they often do not have a dedicated team or deep knowledge on taxability across multiple jurisdictions. Rapid growth across state lines may also result in errors. While sales tax is collected by the vendor, it would ultimately be paid by the customer prospectively. However, this creates a risk of lost revenue if a customer refuses to pay tax or procure services due to additional cost, which generally can be 7 to 8 percent higher with sales tax. The vendor may also be liable for any amount that it had an obligation to collect and report but did not.

- Payroll Tax: The nature of this work often lends itself to large work crews that may travel across state lines and have significant per diems or expense reimbursements. Additional work focuses on nonresident state withholding and controls for traveling employees as well as documentation and support for per diems and expense reimbursements.

- Transfer Tax: For small targets, the transaction is often structured as a true asset acquisition. Asset acquisitions are generally subject to sales tax — including motor vehicle sales and excise tax and real property transfer tax — unless a separate exemption applies. For many facility service businesses, there are significant vehicles that will be transferred as part of the acquisition and transfer taxes may be a significant expense of the transaction. Buyers should focus on evaluating and quantifying any transfer tax that may apply.

- Tax Opportunities: Work Opportunity Tax Credits often apply to large labor workforces and may provide tax savings or benefits for hiring and retention. These tax savings may result in meaningful value to a buyer and help pay for growth.

Consolidation in Facilities Services Will Continue to Grow

The opportunities for PE investors within the Facilities Services sector are abundant, and there's still extensive room for consolidation and good valuation in some subsectors — like janitorial, security, roofing, electrical and plumbing — according to investment banking advisors TM Capital.2

Some subsectors have had very little PE deal activity while some are at very favorable valuation multiples compared to others. Thorough evaluation of the target acquisition's unique business environment, recurring revenue streams and geographic contexts are needed to select the right company to add to a portfolio company's mix.

PE investors with knowledge of the sector and a nose for adding value through efficiencies, technology and leveraging different services under one brand will be rewarded.

Footnotes

1. https://www.mordorintelligence.com/industry-reports/facility-management-market.

2. 2023 Facility Services Report, TM Capital.

Originally published by 02 April, 2024

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.