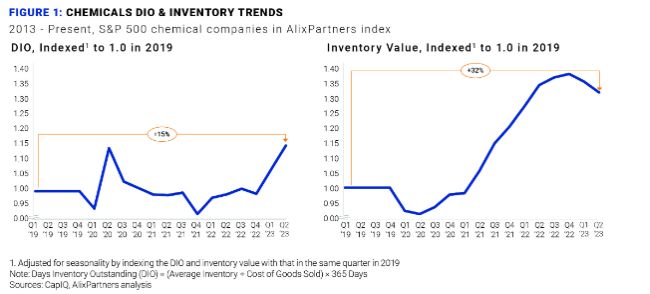

Chemical industry inventory levels soared to record highs over the past quarter, raising the urgent need for a "great destocking." AlixPartners estimates it will take as many as 300 days to reset to sustainable levels.

This development emerges amid reduced demand, constrained borrowing conditions, and headwinds related to company valuations. It is against this complex backdrop that executives should analyze several available levers and implement an action plan.

How did we get here?

Not long ago, the industry was riddled with bottlenecks and stock-outs stemming from several COVID-19-era factors, including unprecedented port congestion. This led to artificial demand inflation, caused by an overbuy of raw materials and other feedstocks.

Supply lanes returned to more normalized conditions faster than companies did. Demand was overestimated and, in the process, capacity needs were miscalculated. As a result, the entire value chain – from raw material suppliers all the way through to formulators, compounders, distributors, and packaging companies to retailers – is holding too much inventory.

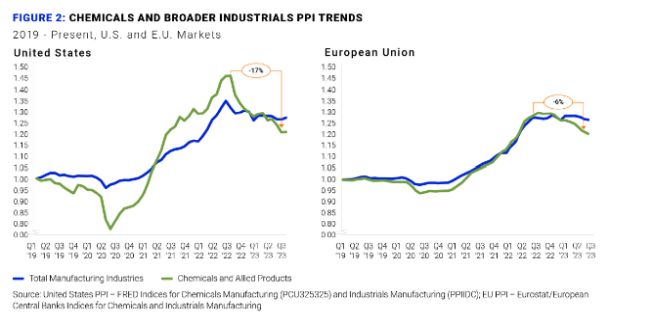

Interest rates remained low through 2022, limiting the cost of working capital. With rates now soaring to a 22-year high, pressure is on to reduce overall working capital. At the same time, the Russia-Ukraine crisis dampened European demand, while driving energy cost escalation. Adding to the pain is the fact that chemical and broader industrial producer prices have been in decline since mid-2022 in both Europe and the U.S.

Companies understand that what goes up must inevitably come back down. To avoid continuing to feed an inventory glut, chemical customers reduced orders from companies providing feedstocks. Chemical companies require accelerated strategies that cover both short- and long-term cashflow – the impact of the inventory run-up and the urgency to act, however, varies across the chemical value chain.

Base chemical and polymer players are relatively less impacted due to the essential day-to-day nature of their products (films, packaging, and consumer goods). Impact on specialty stocks, meanwhile, has been higher due to use in more non-durable heavy applications (agriculture, healthcare, automotive, and construction).

Several high-profile reductions in earnings guidance were announced in mid-2023 – including FMC, BASF, and Westlake – due to destocking. The outlook, meanwhile, isn't pretty. Specialty chemical companies are reducing 2023 demand forecasts by 10 % to 30% vs. original 2023 plans.

THE $140 BILLION TASK

The combined specialty chemicals segment needs reduce at least 45 days of inventory – equivalent to over $140 billion in value – to reach comparable 2019 levels. Swift and decisive action will gird companies against structural headwinds, including declining demand, over-supply in China, and increased competition.

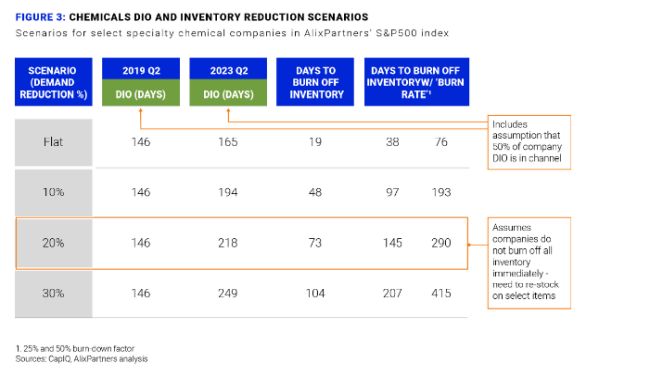

Companies cannot perfectly burn down inventory directly with demand because of several factors. For one, non-productive inventory is drawn down more slowly or not at all. Producers must make trade-offs between inventory reduction targets, operational reliability, revenue, and fixed cost absorption.

At the same time, there is a run-up against shelf-life constraints, leading to potential disposal and write-downs. Companies also maintain inventory in multiple locations due to footprint constraints. Adding to the balancing act is the fact companies will run short on raw materials and need to buy minimum order quantities.

QUICK WINS

We see several potential levers that can be pulled in the near-term, including

- A key strategy to immediately attack the problem is to identify monetization options for obsolete and slow-moving inventory (OSMI).

- For inventory with irregular demand, companies should evaluate manufacturing strategies that shift from Make to Stock (MTS) to Make to Order (MTO) or Configure to Order (CTO).

- The current chemicals market environment provides a robust opportunity to capture raw material 'deflation dividends' associated with lower-cost commodity feedstocks, which will flow into inventory.

- Companies should reset customer and supplier lead times and associated variabilityto reflect current supply chain realities.

- Managers need to recalculate forecasts for the remainder of 2023, and revisit customer lead time commitments to reflect profitability performance.

For more sustainable change, chemical companies should take pursue structural changes that improve supply chain efficiency and effectiveness over the long haul. These actions include:

- SKU rationalization: Companies typically generate all their EBITDA on only a subset of their customers and products. Sunset underperforming products, adjust pricing, and/or standardize raw inputs that drive complexity without improving profitability.

- Manufacturing strategy: The proliferation of contract development and manufacturing organizations allows companies to choose which technologies to maintain internally or outsource to third parties.

- Channel management: Evaluate distributor models where third parties take on inventory responsibilities in non-core regions.

- Strategic sourcing: Procurement departments should evaluate potential suppliers based on lead times, seeking to co-locate the raw material procurement with manufacturing activities.

- Footprint rationalization: Revisit manufacturing networks, seeking to co-locate raw material supply with internal manufacturing in low-cost regions.

- Forecast accuracy: Find opportunities to use Mean Absolute Percentage Error (MAPE) approaches to evaluate forecast accuracy; utilize AI for a market-driven check on bottom-up commercial forecasts.

- Supply chain financing and custody transfer: Evaluate financial partners to defer payment and accelerate cash collection associated with existing supply chain activities. Re-evaluate International Commercial Terms to optimize custody transfer.

- Reliability: Find opportunities to improve overall equipment effectiveness (OEE) and reduce yield loss on key unit operations to prevent the generation of off-spec inventory.

- Digital visibility tools: Adopt digital tools to ensure real-time visibility of inventory.

A LOOK AHEAD

Reducing chemical company inventory is one of the critical issues for chemical company management teams and investors in 2023. More prudent inventory management supports redirecting cash to higher return research & development, M&A, and growth CapEx uses.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.