Following a lull in M&A activity in recent years, the chemical industry is poised to see a potential spike in transactions in 2024. Chemical companies globally have entered a period of increasing margin pressure, boosting the urgency to look for levers to reduce costs, capture market share, and improve competitiveness. Acquisitions and divestitures play a key role in achieving these performance improvement ambitions.

The high cost of borrowing, which was a roadblock to deal-making in 2022-2023, could ease amid an anticipated pause or potential rewind in monetary policies. While economic drivers and market outlooks vary across the chemical industry, we see specific industry sectors with high consolidation potential—namely building & construction, and CASE (coatings, adhesives, sealants, elastomers). While consolidation opportunities exist across all market sectors, executives and investors need to have a playbook to prioritize acquisition/divestiture opportunities and successfully navigate the M&A journey to realize full value potential. This article provides a perspective on historical M&A trends in the chemical industry, an overview of sectors with high consolidation potential, and guidance on where to play and how to win.

Deal volume poised to grow

Chemical companies experienced record revenue and profit growth in 2022, followed by a challenging set of circumstances in 2023 and early 2024. Demand stumbled when destocking, energy and feedstock cost challenges arose, and an imbalance in demand and supply emerged, especially for companies that added capacity in recent years in anticipation of continued growth that failed to materialize. High interest rates added further cost pressure. As a result, profitability has declined across the chemical industry.

Market turbulence has historically led companies to reassess growth strategies. In previous market down cycles, consolidation proved an effective avenue to regain cost competitiveness and market share, while achieving technology synergies.

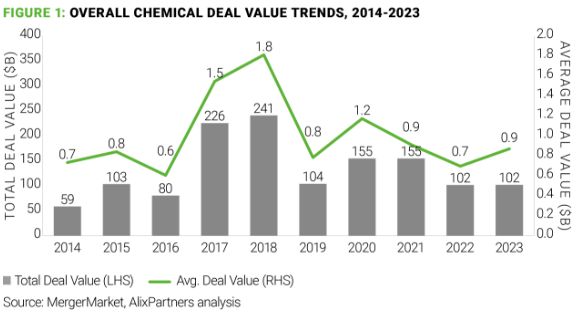

The average deal value peaked during the most recent consolidation surge of 2017-2018, driven by several mega-mergers across the agrochemical, industrial gas, and diversified chemicals market segments. M&A activity, however, has fallen to less than 50% of levels enjoyed during that peak. Rising interest rates have affected both deal volume and transaction values.

M&A momentum began picking up in the second half of 2023, highlighted by ADNOC's bids to acquire stakes in Braskem and Covestro, as well as IFF's interest in divesting its pharma solutions business. Private equity (PE) firms have also been actively driving chemicals M&A activity, with examples in recent years including Advent's sale of Allnex to PTTGC Group; Air Liquide's sale of Schülke to EQT, which subsequently sold it to Athos, a Munich-based family office; and Platinum Equity's combination of Solenis and Diversey into a leading player in water management and hygiene.

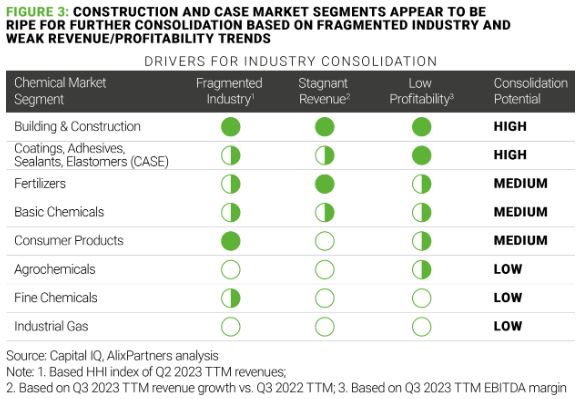

Looking ahead to 2024, M&A activity is likely to further accelerate as companies continue to experience margin pressure, while liquidity begins to recover. We assessed consolidation potential of various chemical market sectors across three drivers:

- Market fragmentation

- Revenue stagnation

- Profitability decline

As the availability of capital improves, market segments with higher fragmentation and revenue/profit headwinds are more likely to consolidate in pursuit of revenue growth, market share capture, and operational efficiencies.

There are two sectors in particular with a higher likelihood of further consolidation:

Building and construction

Chinese building and construction chemical companies, under pressure amid a sharp slowdown in China's property market, are in search of new markets for lower-priced exports for related materials. This represents a revenue and profit headwind for the highly fragmented building & construction sector.

European players reliant on energy-intensive processes, such as inorganic pigments and isocyanates, are disproportionately vulnerable to low-cost Chinese imports. For companies impacted by these market dynamics, M&A may be an attractive strategy, allowing them to diversify geographically, divest from uncompetitive assets, or pursue operational synergies to remain cost competitive.

In addition, tighter environmental regulations for building & construction chemical production are expected to drive consolidation, as large market leaders will be more easily able to develop or acquire new technologies to meet new regulations, while smaller companies may gradually be acquired by the market leaders.

CASE

The coatings, adhesives, sealants, and elastomers (CASE) segment faces similar revenue and profit headwinds to those of the building & construction segment due to overlapping market exposure. There has been a steady level of consolidation activity in the CASE segment throughout the past decade as the industry gradually consolidates. Notable recent acquisitions including PPG's acquisition of Ennis-Flint, Wörwag, and Tikkurila in 2020-2021, as well as AkzoNobel's acquisition of Grupo Orbis, and Sherwin-Williams' Chinese architectural paint business in 2022-2023.

However, CASE remains a fragmented sector, and further consolidation is expected to continue as market leaders acquire smaller players to diversify their product offerings. While European CASE companies were popular acquisition targets in the past due to relatively higher industry fragmentation, high energy prices in the region have subdued interest in European assets and companies. Historical M&A trends may reverse as Europe-based CASE companies seek acquisitions in other regions to diversify their market and asset footprints.

Private equity role in chemical industry consolidation

Private equity firms are expected to continue playing an active role in driving chemical industry consolidation. They may seek value creation by targeting non-core businesses of chemical companies, which lack management attention and cost transparency. Value creation levers that PE owners typically pull include cross-selling, go-to-market, salesforce effectiveness, and partnerships to realize commercial synergies, as well as general and administrative (G&A) reduction, direct and indirect procurement, and manufacturing optimization (e.g., yield improvement; footprint optimization). Management changes and digitization using machine learning and artificial intelligence are common tactics PE employs to drive rapid value creation.

PE-driven market consolidation is also an important motivator that PE funds will use to grow the top line and realize revenues and cost synergies. Take, for instance, the carve-out of Kersia, a hygiene chemical company from the French Groupe Roullier. Over the course of PE fund Ardian's tenure, Kersia's revenue grew to more than three times its pre-acquisition value. ESG is another focus area, with PE firms pulling ESG levers to reduce cost via both material and energy savings, while also growing the top line by entering new "green" product categories.

PE funds will be quite selective in such transactions. They may prioritize non-cyclical businesses that have high barriers to entry, limited threat of Chinese competition, and are operating in markets with strong growth drivers and the potential to consolidate through acquisition.

Adopting a strategic approach

Despite the expectation of a pickup in M&A activity, companies and investors alike need to be cognizant of key M&A success factors and pitfalls, and remain actively engaged across the full M&A deal cycle to capture the full synergy potential. A strategic roadmap to navigate an M&A transaction should include the following considerations:

1. Begin with the end in mind.

Set clear objectives and ensure the M&A strategy aligns with long-term goals. At the same time, assess cultural compatibility between the acquirer and target companies. A good cultural fit can accelerate post-merger integration.

2. Clearly define revenue and cost synergies and identify roadblocks.

Financial, operational, legal, and regulatory due diligence performed over cross-functional teams will spotlight areas of concern and opportunity. Risks include antitrust regulations, operational integration, customer retention, supplier disruption, debt obligations, cybersecurity and ESG. Synergies, meanwhile, include portfolio diversification and cross selling, channel partnerships route-to-market access, direct and indirect costs, and technology and R&D benefits.

In the case of carveouts, companies should also evaluate: Length and price of Transition Service Agreements (TSAs); G&A services such as IT, HR, and finance; potential innovation; and resources and tools needed.

3. Create a robust implementation plan.

- Integration planning: Clearly define teams, milestones, timelines, and KPIs; drive alignment throughout the process.

- Change management: Develop a clear and transparent change and communication plan that covers internal and external audiences. Involve employees early on, effectively articulate changes, and cast a clear vision for what the combined entity is driving towards.

- Rapid implementation: Execute quick-win initiatives to demonstrate a winning strategy and build momentum for integration.

- Technology integration: Comprehensively plan for IT systems and infrastructure integration; data migration should be seamless and not disrupt ongoing operations, and safeguards should be established to ensure data security.

4. Build for post-merger success and continuous improvement.

Conduct a thorough review of integration efforts to not only evaluate success, but to identify areas for improvement. Continued monitoring of value creation, the implementation of continuous improvement processes, and lessons learned provide the foundation for sustained business performance improvement.

By focusing on these considerations and taking a strategic, well-executed approach, chemical industry players can increase the likelihood of a successful M&A outcome, fully realize the synergies envisioned during the integration process, and be well-positioned to thrive in an ever more competitive market environment.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.