What is PPT?

Plastic Packaging Tax (PPT) became effective in the UK on the 1st April 2022 as part of the government's Resources and Waste strategy, aiming to encourage businesses to use recycled plastic in packaging and reduce plastic waste.

HMRC states that "the aim of the tax is to provide a clear economic incentive for businesses to use recycled plastic in the manufacture of plastic packaging, which will create greater demand for this material. In turn, this will stimulate increased levels of recycling and collection of plastic waste, diverting it away from landfill or incineration."

Businesses that manufacture or import 10 tonnes or more of plastic packaging within a 12 month period have to register to pay PPT; currently at a rate of £210.82 per tonne (2023 tax year) on plastic packaging components with less than 30% recycled plastic that are manufactured or imported into the UK.

The Gov.uk website provides an overview of which packaging is classified as plastic packaging, as well as having access to an online assessment form to assist with deciding if you're required to pay PPT and if so, how much.

Upcoming Changes to PPT

In the Autumn Statement 2023, the government announced that the rate of PPT would increase in line with the Office for Budget Responsibility (OBR) forecast of Consumer Price Index (CPI) inflation. The rate of PPT will increase to £217.85 per tonne and will apply to all plastic packaging, containing less than 30% recycled plastic that is manufactured and imported into the UK on and after 1 April 2024. The measure is not anticipated to have a significant financial impact on individuals, households, and families due to its increase aligning with the inflation rate.

Has PPT been effective thus far?

With PPT being recently introduced to British manufacturing businesses, first announced in 2018 and introduced in 2022, it is worth focusing on the impact that PPT has had on businesses thus far using HMRC's released data.

PPT receipts in the financial year 2022/23 amounted to £276 million, with HMRC initially predicting revenue of £235 million. As of 8th August 2023, 4,142 businesses had registered to pay PPT, whilst HMRC had initially predicted 20,000 manufacturers and importers would qualify. The data supports the need for either better enforcement of the scheme, or greater awareness of PPT.

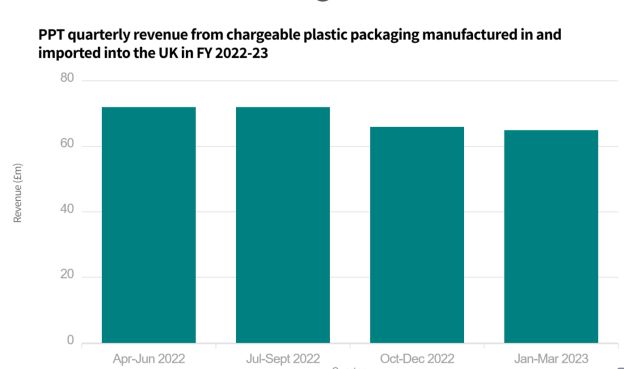

PPT is still in the introductory stages and is therefore difficult to label as successful or unsuccessful just yet, HMRC data reveals that PPT revenue has been marginally decreasing each quarter (Figure 1), and could prove effective if observed over a longer period of time as more businesses move to sustainable materials options and reduce their reliance on plastic.

Figure 1

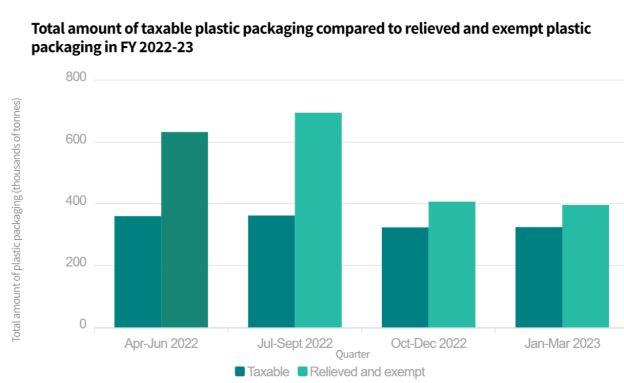

Figure 2

(Data collected from statistics published on the HMRC website.)

However, in comparison to exempt packaging, which has declined drastically in the last two quarters, figure 2 shows that the tonnage of taxable plastic packaging has remained relatively consistent. This consistency of taxable packaging supports the Government's (April 2024) increase in the rate of PPT in line with Consumer Price Index (CPI) as the scheme could be more effective in order to deter more manufacturers from using plastic packaging.

Patrick Brighty, recycling policy advisor at Environmental Services Association, agrees that the 'Government must look to apply a long-term escalator to the PPT- increasing both the tax rate and the minimum recycled content threshold over time.'

To similar effect, a Carbon Border Adjustment Mechanism (CBAM) is set to be implemented in 2027, further details on the design and delivery of a UK CBAM will be subject to consultation in 2024. Under the mechanism, it is proposed that the charge applied on imported products will depend on the carbon emitted in the production of the imported good. The scheme aims to contribute towards the goal that the UK will be carbon neutral by 2050 and aims to see businesses making carbon efficient choices when importing products.

How do I pay my PPT return?

Once you have registered to pay PPT, you must submit a return and pay any tax due by the last working day of the month after the end of the tax period. Your return must cover an accounting period, with the next accounting period beginning, 1st January to 31st March 2024 and the deadline being the 30th April 2024.

Tax returns can be submitted on the Gov.uk website using your Government Gateway User ID and password which would have been given to you when you first registered for tax. We advise you keep records of which packing and components you must pay PPT on, the weight of the package you import, and a record of your accounts to make the tax return process easier to manage.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.