Jonathan Jex - Jex Capital Allowances

Jonathan of JexCA explains how pre-contract enquiries are often misleading and the pitfalls of not scrutinising the replies

CPSE is the best practice approach to seek information and clarification on a range of matters during the pre-contract negotiation process. In CPSE.1 (version 4.0) General pre-contract enquiries for all commercial property transactions, capital allowances are dealt with under 33.1 to 33.11. The replies are the starting point for the buyer's capital allowances pre-acquisition due diligence, however, the replies are often less than adequate.

We regularly see "there are no capital allowances available" or "the capital allowances are not being sold" or "the seller is retaining the right to claim capital allowances" or often "not applicable". The entitlement to claim capital allowances rests with the holder of an interest in land and transfers automatically to the new owner when property is sold.

CPSE 33 seeks to establish how the property is held by the seller, whether they have claimed capital allowances and/or entered into any agreement with a prior owner, and whether they are agreeable to meeting the pooling and fixed value requirements.

Often we see replies that make us chuckle, but in reality these are worrying as so many people do not challenge the replies and accept them at face value, for example:

One would have thought that 33.1 would be the easiest enquiry to answer as all commercial property will be held either on capital account as a fixed asset or as trading stock. Here are some replies we have seen

33.1 Do you hold the Property on capital account as an investor/ owner-occupier, or on revenue account as a developer/ property trader as part of your trading stock? Please specify which

- No

- N/A

- Not applicable for occupiers

- No enquiry has been made and the Buyer should rely on its own enquiries

- The Seller does not see the relevance of this section 33 as it is not an industrial building

The following is a recent example of replies we received to 33.1, 33.2 and 33.3

33.1 Do you hold the Property on capital account as an investor/ owner-occupier, or on revenue account as a developer/ property trader as part of your trading stock? Please specify which

Trading

33.2 Have you claimed capital allowances on plant or machinery fixtures or allocated any expenditure on such fixtures to a capital allowances pool? If so, please answer the supplementary questions in enquiry 33.9 in respect of that expenditure

Yes

33.3 If there is any expenditure on plant and machinery fixtures that you have not pooled, etc. No expenditure has been pooled

The reply to 33.1 advises that the property is held as stock, meaning there is no entitlement to claim. However, 33.2 advises that capital allowances have been claimed, then 33.3 says that no expenditure has been pooled, i.e. no claims have been made. The replies to these first 3 enquires contradict each other entirely.

Another common reply when asked to list fixtures that have been claimed is to state a washing machine, tumble drier or motor car, clearly not fixtures falling with CAA 2001 s173. When carrying out pre-acquisition due diligence the replies to CPSE is not the end of investigations, merely the beginning, never accept at face value a reply such as "there are no capital allowances available". The statement may well be correct, but you need to know why and not just accept it.

The number of times we have heard that statement where the actual position is the opposite are too numerous to list.

Recently our client's solicitor advised "the seller's solicitor has confirmed there are no capital allowances available...maybe you thought you would get some and that informed your offer, hope not". Thankfully rather than accept that response the client referred to us to undertake our own due diligence.

Clearly from the outset our client had an entitlement to claim as the sellers had acquired pre April 2008. We asked for an explanation why there were no allowances available to which they replied, "why can't you just accept there are no allowances and let your client exchange contracts, you are holding up the transaction".

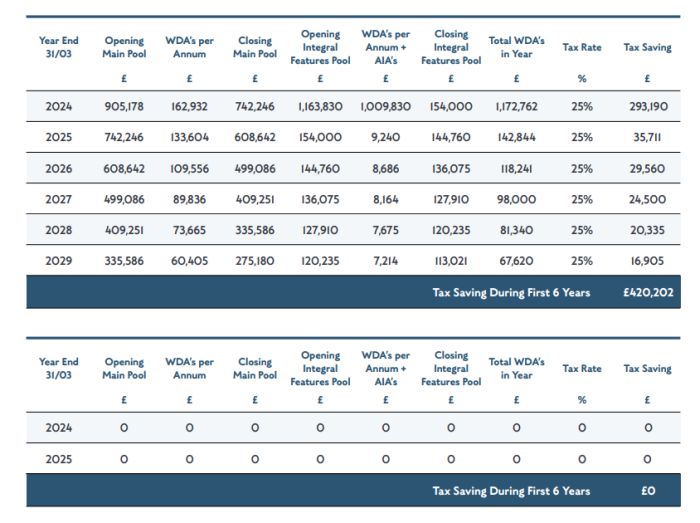

The property had been constructed and held by a pension fund who sold to an investor with a s198 joint election at £1, clearly this election was invalid and of no effect. However, the investor thought they couldn't claim capital allowances and also that they had to elect at £1 when they sold. The purchase completed without any election and our client was able to claim capital allowances of £1.4m on the acquisition of a regional office for £4m and providing tax relief in the region of £266,000, much of which was available in the first year utilising annual investment allowances.

"CPSE is the best practice approach to seek information and clarification on a range of matters during the pre-contract negotiation process.

Fortunately our client was well informed enough not to accept the advice given but to refer to a capital allowances specialist. I am sure though that many transactions proceed based upon incorrect replies to CPSE 33 and many opportunities for Buyers to claim tax relief goes unutilised.

The replies to CPSE are not the end of the capital allowances due diligence but the beginning. The replies should be drilled down into to ascertain why they are saying what they are and further enquiries made specific to the current transaction, as each transaction will have a different capital allowances position.

The following tables show the potential flow of tax relief for a property acquisition where specialist advice was taken and where it was not taken. Please don't be the latter!

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.