One of the many benefits enjoyed by wealthy individuals is the ability to own multiple residences. Often, the second residence is located in a resort location where significant rental income may be possible. Generally, the owner of the second residence is able to deduct the mortgage interest and the real estate taxes regardless of whether the property is rented. However, the interest deduction may be limited because the combined mortgage balance exceeds the $1.1 million limit and the real estate taxes may be limited if the taxpayer is in the alternative minimum tax (AMT).

There is a very complex set of tax rules that govern the treatment of second residences that have both personal and rental use. For example, if the personal use is less than the greater of 14 days or 10% of the rental days, then the personal use is ignored and the second residence is treated as a rental property, with all expenses being deducted on Schedule E. Conversely, if the second residence is rented for less than 15 days, the rental income is ignored and the residence is treated as a personal residence with the mortgage interest and real estate taxes being treated as itemized deductions on Schedule A subject to the limitations noted above. If the personal use and the rental use each exceed 14 days, then the property is treated as a "vacation home" and the expenses must be prorated between personal and rental. In effect, this allows you to exceed the $1.1 million limit on personal mortgage interest deductions and the potential AMT problem with the real estate taxes.

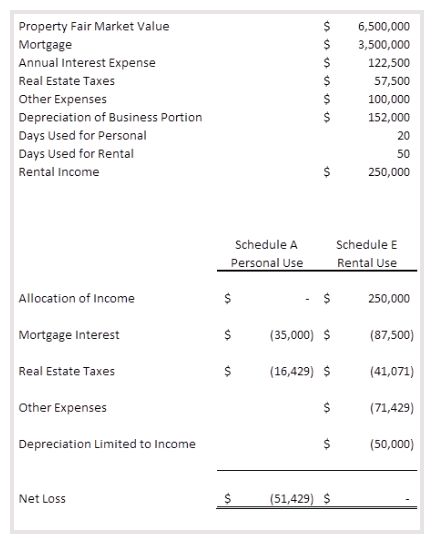

With respect to the rental portion of the property, there are very strict ordering rules and limitations on the rental deductions. Under the ordering rules, mortgage interest and real estate taxes are deducted first, additional expenses other than depreciation are second, and depreciation is third. Overall, the deductions may not exceed the income in any year, but any excess deductions carry over and may be used if and when the property is sold. An example follows:

With proper structuring, the $1 million personal mortgage interest limitation is no longer at issue and you have improved the overall economic performance of the property.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.