1. On 31 July 2012, a mere two months after the General Court handed down its judgment in the MasterCard case, the European Commission (the "Commission") sent a supplementary statement of objections ("SSO") to Visa in relation to the multilateral fall-back interchange fees ("MIFs") it charges for transactions with consumer credit cards in the European Economic Area ("EEA") and domestic point of sale transactions in eight EU Member States.

2. According to the Commission: "Visa's credit and debit cards represent approximately 41% of all payment cards issued in the EEA. Visa has the largest acceptance network within the EEA with over 5 million merchants accepting its payment cards. In 2010 a total of 35 billion card payments were made in the EEA, with a total value of €1800 billion."

The SSO of 2012

3. The Commission's preliminary view in its SSO is that VISA's MIFs effectively fix a minimum price for the merchant service charge ("MSC") levied by the banks on retailers and restrict competition between banks contrary to Article 101 (1) of the Treaty on the Functioning of the European Union ("TFEU").

4. The Commission also doubts once more whether the Visa MIFs satisfy the exemption criteria set out in Article 101(3) TFEU1 in that the MIFs do not appear to be necessary for technical or economic progress and any benefits from the restriction are not passed down to retailers and consumers. Furthermore, the Commission considers that Visa's rules requiring cross-border acquirers to pay MIFs applicable in the country of transaction restrict trade between Member States and support the division of European markets across national boundaries.

Background

5. The investigation into Visa's payment card scheme stretches back many years. Visa originally notified its international payment card system to the Commission in 1977. Twenty five years later2 and in response to undertakings offered by Visa (the "2002 undertakings")3, the Commission exempted Visa's cross-border MIFs4 under Article 81(3) of the EC Treaty (now Article 101(3) TFEU). The exemption decision related to payments made with consumer credit cards, deferred debit cards and debit cards. The 2002 undertakings expired in December 2007.

6. In March 2008, the Commission began an investigation into Visa's MIFs for consumer debit and credit cards. The Commission sent a statement of objections ("SO") to Visa in April 2009 and in December 2010 accepted undertakings offered by Visa EUROPE in relation to debit card transactions (the "2010 undertakings"). The commitments offered are for four years expiring on 8 December 2014.

7. The 2010 undertakings were only in relation to debit card transactions. Consequently the Commission remained free to initiate or continue proceedings in relation to commercial credit card transactions, and deferred debit cards. The SSO issued in July 2012 relates only to consumer credit cards.

How does the MIF work?

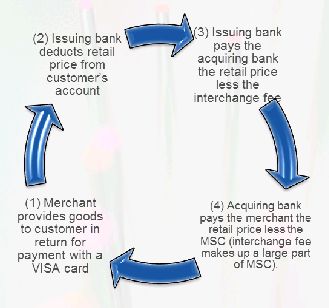

8. A MIF is an interbank payment made for each transaction with a payment card. A merchant will provide goods to a consumer in return for payment with a Visa card. The customer's bank ("issuing bank") then deducts the retail price from the customer's account. The issuing bank then pays the retailer's bank (the "acquiring bank") the retail price less an interchange fee (a service fee for managing the card system). The acquiring bank then pays the merchant the retail price less a merchant service charge ("MSC") a large proportion of which is made up of the MIF. The operation of the system is shown diagrammatically below.

9. Multilateral fall-back interchange fees (i.e the MIFs) are agreed in the absence of a bilateral agreement as to the interchange fee between the issuing and acquiring bank.

10. The MIF is set by the Visa Board whose members comprise a number of banks.

The Commission's case against Visa Europe

11. In its 2009 SO, the Commission identified an upstream network market where the payment card schemes compete with each other to persuade financial institutions to sign up to their scheme and where payment card schemes provide services to those institutions in return for a fee. The Commission also identified a downstream issuing market (where financial institutions issue payment cards to card holders in return for a fee) and a downstream acquiring market (where financial institutions accept card payment for merchants in exchange for the merchant service charge).

12. The Commission expressed concerns in its SO that Visa Europe's MIFs were the result of a decision of an association of undertakings (the credit institutions which make up the Visa board) or an agreement between undertakings which restricted competition in the acquiring market as it "inflate[d] the base on which acquirers set the merchant service charge by creating an important cost element common to all acquirers"5This was detrimental to merchants and consumers. The Commission considered that the MIFs were not objectively necessary to the payment scheme and that the restrictive effect was exacerbated by other network rules such as the honour all cards rule,6 and the no- discrimination rule.7 The Commission did not consider that the MIFs satisfied the criteria set out in Article 101(3) TFEU.

What undertakings were offered in 2010 in relation to debit cards?

13. Visa offered to:

a. Cap its yearly weighted average cross-border MIFs applicable to transactions with its consumer debit cards at 0.2%. The cap also applies in each of the EEA countries where Visa Europe directly sets specific domestic debit MIF rates and in those countries where cross-border MIFs apply in the absence of a bilateral agreement between the acquiring and issuing bank. (The cap of 0.2% accepted by the Commission can be modified by agreement between the Commission and Visa Europe if more reliable data for calculating the MIF rates based on the merchant indifference test ("MIT") ?] becomes available after the Commission concludes its study on the costs and benefits to merchants of accepting different payment methods).

b. Continue to implement and improve transparency introduced by the Visa Europe Board in March 2009.

Looking back: how do Visa's undertakings in 2002 and 2010 compare?

14. Cap on the MIF: In 2002 Visa agreed to progressively reduce the level of the MIF for credit cards, debit and deferred debit cards from an average of 1.1% to 0.7%. These were found to be an acceptable level. In 2010, the Commission accepted a cap on the yearly weighted average cross-border MIF of 0.2%.

15. Although this may seem to suggest that the Commission has taken a stricter approach to the level of the MIF than might satisfy the exemption criteria in Article 101(3) TFEU, it may be more a reflection of the Commission's developing thinking in relation to the MIT or the "tourist test" which was the test used as a basis for the calculation of the MIF in both the VISA 2010 undertakings and the undertakings offered by MasterCard in 2009.

16. This test is based on studies conducted by central banks in a number of EEA countries which compared the costs to retailers of accepting payment with cards as opposed to payment with cash. According to the MIT, the appropriate level of the MIF is the level at which merchants are indifferent to whether they receive payment with cash or a card. For this to occur, the merchant must not pay more than the cost savings it receives from receiving payment with a card (such as reduced transportation or security costs compared with the use of cash or a reduction in check-out times at cash desks). Depending on the extent to which this charge is passed onto cardholders, transparency in the level of the MIF will allow cardholders to make informed choices as to which payment instrument provides the better value, thereby increasing competition between payment instruments.

17. Transparency: both sets of undertakings involved a commitment to increase transparency of charges made to the retailer. In particular the 2010 commitments provide for an unblending of the MSC, the registration and publication of all MIF rates and the full visibility and electronic identification of commercial cards as well as the possibility for merchants to choose whether to accept Visa, Visa Electron or V Pay cards. The 2010 commitments contrast to the 2002 commitments where the transparency requirement merely required member banks to disclose to retailers who requested such information their MIF levels as well as the relative percentage of their costs for providing services such as the free funding period, payment guarantee and transaction processing. The new commitments require active publication of the charges such that transparency is guaranteed rather than being reliant on the retailer requesting the information.

Looking forward

18. On the 11 October 2012, it was reported in the press8 that the Commission had received proposals from VISA to allay its competition concerns. If this is true, it will continue VISA's strategy of offering commitments to avoid fines. If undertakings are accepted by the Commission, then this will at least remove some of the legal uncertainty over MIFs which has dogged this industry for decades, and, in its own way caused barriers to innovation and cross-border trade. The industry will still have to wait for the outcome of the MasterCard case which has been appealed to the Court of Justice of the European Union ("CJEU"). Judgement by the CJEU is unlikely to be handed down for a few years.. It is unclear whether the OFT will issue a decision in its MasterCard investigation (which analyses domestic MIFs)before the CJEU's judgement is handed down. This is because the result of that judgement of the CJEU will impact on the OFT's case. Consequently the legal uncertainty experienced in this sector for so many years is likely to persist still further.

1. If the judgement upholds the General Court's findings, then will MasterCard offer undertakings to redress the competition issues? If so, any remedy is likely to be judged against the MIT test.

2. Whatever the CJEU decides it is unlikely to be fully in line with previous judgements handed down in different countries in relation to their national MIFs. Therefore even when a judgement is finally handed down, it may not have the desired effect of harmonising MIFs across Member States of the European Union.

3. It is because of this desire and indeed the urgent need identified by the Commission in its Green Paper on Card, Internet and Mobile Payments9 reduce barriers to cross-border payments within the EU, that the Commission issued a Communication on 3 October 2012 which states that it intends propose legislation under the Single Market Act II to "revise the Payment Services Directive and make a proposal for multilateral interchange fees to make payment services in the EU more efficient."10

4. While regulation may finally put an end to the uncertainty which has dogged the charging of cross-border MIFs for years, it remains to be seen whether this will in fact be the panacea it is intended to be.

Footnotes

1 For a restriction to fall within the Article 101(3) exemption criteria, it has to:

"contribute[s] to improving the production or distribution of goods or to promoting technical or economic progress, while allowing consumers a fair share of the resulting benefit..." and must not:

"(a) impose on the undertakings concerned restrictions which are not indispensable to the attainment of these objectives;

(b) afford such undertakings the possibility of eliminating competition in respect of a substantial part of the products in question."

2 During this time the Commission assessed numerous aspects of the scheme and issued a comfort letter in 1985. The investigation was reopened after a complaint about Visa's multilateral interchange fees by the British Retail Consortium and the comfort letter was also withdrawn in 1992. The reopened investigation also took into account a complaint in 1997 about other aspects of the Visa international payment scheme. These other aspects of the scheme were found not to infringe Article 81(1) EC (now Article 101 TFEU) in 2001.

3 The undertakings were as follows:

a) To progressively reduce the level of the MIF for credit cards, debit and deferred debit cards from an average of 1.1% to 0.7% over the period of the undertakings which terminated at the end of 2007; and

b) To cap the MIF at the level of costs for certain services offered by issuing banks i.e. the free funding period, payment guarantee and transaction processing; and

c) To make the payment card system more transparent by allowing member banks to disclose to retailers who requested such information, their MIF levels as well as the relative percentage of the three costs categories (listed above) to retailers.

5 http://ec.europa.eu/competition/antitrust/cases/dec_docs/39398/39398_6930_6.pdf

6 The honour all cards rule obliges the acquiring bank to accept payments made with all valid Visa-branded cards, irrespective of the identity of the issuer, the nature of the transaction and the type of card being issued.

7 The no discrimination rule prevents merchants surcharging for payments made with a Visa card.

8 MLEX

9 http://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri=COM:2011:0941:FIN:EN:PDF For a summary see http://www.kemplittle.com/Publications/item.aspx?ListName=KLBytes&ID=85

10 http://ec.europa.eu/internal_market/smact/docs/single-market-act2_en.pdf, p 18

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.