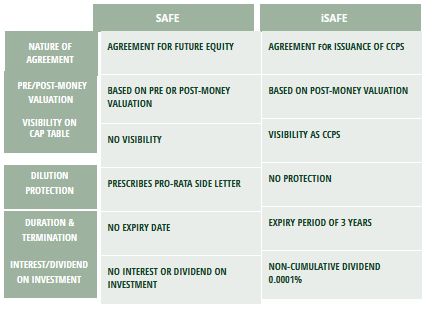

NATURE OF iSAFE & SAFE

iSAFE (or India SAFE) was introduced by an Indian VC firm 100X.VC, as an adaptation of 'SAFE' (or 'Simple Agreement for Future Equity') document originally introduced by US based fund Y-Combinator. Speaking in Indian legal terms, we see the Y Combinator 'SAFE' as a non-expiratory, non-interest bearing 'Memorandum of Understanding for contingent stock issuance' with advance consideration, and contingent re-payment obligations in form of cash or conversion to stocks.

iSAFE IS AN AGREEMENT FOR ISSUANCE OF CCPS

The iSAFE, as we see it, is nowhere similar to SAFE either in form or context. It is rather simply an "agreement for issuance" of CCPS (Compulsory Convertible Preference Shares), which are interest rate bearing, having contingent 'class conversion' obligations on the issuing company, and a definitive date for equity conversion. The 'class conversion' provisions are however somewhat similar or identical to the future equity issuance provisions in the SAFE document. The SAFE document contemplates an 'Equity Financing' event as the trigger point for issuance of preferred stocks whereas the iSAFE hints an event of conversion of class of already issued CCPS to the iSAFE note holder. This is evident from the reading of the definition of Conversion Date in the iSAFE document. The "Conversion Date" is defined as the date on which the iSAFE Notes are automatically converted into the Conversion Shares pursuant to an Equity Financing event. This means that the existing CCPS issued to the iSAFE Note holder at the time of iSAFE execution are cancelled for a new set of CCPS or equity shares. iSAFE is neither debt nor equity, it is somewhere in between the two i.e. is an 'Agreement to issue CCPS'. iSAFE investment may not be considered as 'Debt', but it is still above Equity because of the 'Liquidation Preference' it holds. If the startup fails, iSAFE note investor will always have preference over equity shareholders for return of their iSAFE investments.

SAFE v. iSAFE

SAFE VARIATIONS

The SAFE was initially designed as a Pre-Money Valuation document but later on shifted to a Post-Money Valuation model and currently prescribes three different variations along with a 'Side Letter' for reducing dilution impact for SAFE holders. The documents are:

- Valuation Cap, no Discount

- Discount, no Valuation Cap

- MFN, no Valuation Cap, no Discount

- Pro-Rata Side Letter

Valuation Cap, no Discount

At the time of an Equity Financing (a priced round) the price per preferred stock to be issued to SAFE holder is determined as:

Note: SAFE prescribes that In this case the rights, privileges, preferences and restrictions for such Preferred stock are superior to the Standard Preferred Stock of the company. And the conversion price for price based anti-dilution protection and dividend rights are based on the Per share price.

Discount, no Valuation Cap

At the time of an Equity Financing (a priced round) a discounted price per preferred stock to be issued to SAFE holder is determined as:

![]()

MFN, no Valuation Cap, no Discount

At the time of an Equity Financing event (i.e. priced round) a discounted price per preferred stock to be issued to SAFE holder is determined as Lowest price per Standard Preferred Stock (i.e. Face Value).

Dilution Mechanism through Pro-Rata Side Letter

Since, a single SAFE transaction is an investment round on its own, the ownership of a SAFE holder has to be perceived after infusing investment amount i.e. post-safes and not post-Series A. This means SAFE holders are diluted by the Series A like everyone else. To address this issue, the Y Combinator SAFE also prescribes a 'Pro-Rata Side Letter' document which determines the estimated dilution percentage of the SAFE holder that is going to happen at the Equity Financing event, and entitles the SAFE holders to subscribe for a percentage of the total round equivalent to their as converted ownership or a Safe Pro Rata Allocation Percentage.

COMING BACK TO iSAFE

iSAFE drafters have tried to incorporate SAFE identical concepts and terminologies in their document and they claim it to be even safer document and secure investment route as a legally recognized security instrument in India i.e. CCPS. However, the risks that are associated with any original SAFE document can neither be addressed nor mitigated through this Indian adaptation of SAFE. The real and actual risks associated with these documents are not with respect to their form and nature or the nature of securities issued under them, BUT the risk at the end of Seed Stage Startups of not understanding the nitty-gritties, concepts, conversion formulas, definitions, rights, privileges, preferences and restrictions covered in these documents. Seed stage investors claim iSAFE to be a 'STANDARD' and 'INDUSTRY ACCEPTED' document.

VISIBILITY OF iSAFE ON CAP TABLES

It can be said that the Indian document iSAFE addresses a major issue that rides with the original SAFE that is the non-visibility or non-fungibility of the SAFE investment on the Cap Table of the company. iSAFE drafters claim that this issue is entirely addressed "as the iSAFE notes take the form of legally recognized instrument in India i.e. Compulsorily Convertible Preference Shares (CCPC) and therefore any investment through iSAFE sequel notes is recognized and visible on the Cap Table of the company. While this may seem strikingly beneficial for the investor, it hardly makes any difference in terms of enforceability and maintainability of either the SAFE in its original form on one hand or the iSAFE i.e. agreement for issuance of CCPS.

CAN SAFE DOCUMENT BE IMPLEMENTED IN INDIA?

There is much ambiguity for a definitive answer to this question. Especially when SAFE adaptations are fairly new to India and the Indian regulators. There are a lot of apprehensions on the legality, recognition and enforceability of the SAFE document if implemented in India. Some may argue that since a SAFE is neither a 'Equity Instrument', a 'Security or Debt instrument'', 'Convertible Note' or other, the SAFE holder will have no downside protection over their SAFE investments. From the startup investee company standpoint, the SAFE investment can never force a startup to recognize the SAFE investment amount in their books and disclosure as 'Debt'. This was the entire idea and charm of a Simple Agreement for Future Equity, that is, to raise money at seed stage when no definitive value can be ascertained for a startup idea and convert the amount into equity or preferred stock in the event of a priced equity round or a Series A.

POSSIBLE MODE OF IMPLEMENTATION OF SAFE DOCUMENT

SAFE document in its form can be seen as a shorter and standardized form of an SSA (Share Subscription Agreement) with a contingent 'closing date' and no expiry. Entire investment amount can be considered as advance sale consideration paid upfront to the idea stage startup and this contingent SSA can be enforced like any other agreement to perform certain obligations. Admittedly in the event of a dispute, the investment amount may not be seen by the courts as 'Debt' but the obligations relating conversion, cash-out, liquidation and pro-rata dilution may still be enforceable like any other contract, SSA/SHA or SSSHA. From a commercial and investor point of view, such high risk investments are never thought of as Debt at the time of investment.

FUTURE OF iSAFE IN INDIA

A lot of deliberations sensitization over this topic is required in India at the founder and entrepreneurial level. It would be totally incorrect to say that the iSAFE document is going to obviate the need of long agreements viz. SHA (Share Holder Agreements), or that it dispenses the need for corporate legal review by a competent and domain expert lawyer, or that the terms of iSAFE are outrightly favourable for entrepreneurs.

Originally published 13 November 2021

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.