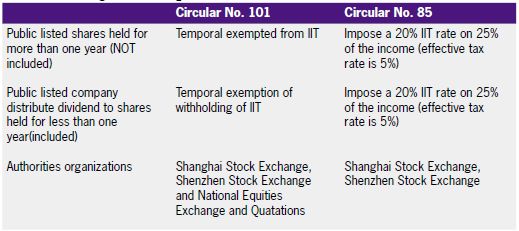

Following the publication of Caishui [2012] Circular No. 85 (hereinafter referred to as Circular No. 85):

Notice on Certain Issues Concerning Implementing Differential Individual Income Tax treatments for Dividend and Bonus Obtained by Individuals by Holding Shares in Listed Companies, on Sep. 7, 2015, Ministry of Finance of People's Republic of China, State Administration of Taxation and China Securities Regulatory Committee again jointly issued [2015] Circular No. 101 (hereinafter referred to as Circular No. 101): Notice on Certain Issues concerning Differential Individual Income Tax Treatments for Dividend and Bonus Obtained by individual by Holding Shares in Listed Companies to clarify individual income tax treatment for dividend and bonus obtained by holding shares in listed companies. This adjustment of policy intends to bring the guiding role of taxation policy into better play, encourage long-term investment, restrain short-term speculation and promote the long-period stability and prosperity of the national capital market.

Key points of Circular No. 85

Key adjustments:

Compared with Circular No. 85, Circular No. 101 has introduced the following new tax preferences:

The practical details would be the same as these outlined in Circular No. 85.

Effective Date

The Circular No. 101 would be applicable to the shares obtained and registered later than 8 Sep, 2015. If the shares are already recorded in an individual investors' securities account on the effective date of this circular, the holding period shall be calculated from the date of obtaining the shares.

Our observations and suggestions

1. During the past three years, Circular No. 85 has been practiced and afforded rich experiences for launching Circular No. 101. Compared with Circular No. 85, we noticed that Circular No. 101 differs in the following aspects:

- Provide further IIT exemption on dividend derived from shares held for more than one year (not included);

- Clarify IIT preference on dividend would also applicable to the shares listed on National Equities Exchange and Quatations;

- Simplify the taxation process for the shares held for less than one year (included)

2. The introduction of Circular No. 85 and No. 101 shall not affect the IIT exemption on income due to transfer of shares in listed companies.

3. With more tax exemption available for IIT on dividend, we would suggest the investors and the taxpayers to perform efficient and practical planning when disposing their assets to mitigate the tax burden while stay compliance with the tax regulations.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.