After almost two years following its proposed rules, on March 6, 2024, the Securities and Exchange Commission (SEC) adopted final rules to require public companies to disclose certain climate-related information in registration statements and annual reports.

The SEC proposed the rules on March 21, 2022, and subsequently received over 24,000 comment letters. The SEC was responsive to the exceptional amount of outside commentary. At over 800 pages, the adopting release far exceeds the length of the proposing release, but the final rules are narrower in scope and utilize a less prescriptive approach than the proposed rules. The SEC chose to significantly modify or eliminate some of the most controversial elements of the proposed rules, including most notably (and predictably) dropping the requirement for any Scope 3 reporting.

For an overview of the proposed rules, please see our March 2022 blog post. We detail some of the similarities and differences between the proposed and final rules below.

Consistent with the proposed rules, the final rules require a company to disclose, among other matters:

- Material climate-related risks and activities to mitigate or adapt to such risks.

- Information about a company's board of directors' oversight of climate-related risks.

- Management's role in managing material climate-related risks.

- Information on any climate-related targets or goals that are material to a company's business, results of operations, or financial condition.

In addition, the final rules require:

- Disclosure of Scope 1 and/or Scope 2 greenhouse gas (GHG) emissions by large accelerated filers (LAFs) and accelerated filers (AFs) when those emissions are material.

- The filing of an attestation report covering the required disclosure of those Scope 1 and/or Scope 2 emissions.

- Disclosure of the financial statement effects of severe weather events and other natural conditions, including, for example, costs and losses.

The final rules differ from the proposed rules in many ways, including the following:

- Eliminating the proposed requirement for all registrants to disclose Scope 1 and Scope 2 emissions and instead requiring such disclosure only for LAFs and AFs, on a phased-in basis, only when those emissions are material, with the option to provide the disclosure on a delayed basis.

- Exempting smaller reporting companies (SRCs) and emerging growth companies (EGCs) from the Scope 1 and Scope 2 emissions disclosure requirements.

- Modifying the proposed assurance requirement covering Scope 1 and Scope 2 emissions for AFs and LAFs by extending the reasonable assurance phase-in period for LAFs and requiring only limited assurance for AFs.

- Eliminating the proposed requirement to provide Scope 3 emissions disclosure entirely for all companies.

- Eliminating the proposed requirement to describe board members' climate expertise (similar to the final cybersecurity rules).

- Requiring disclosure of material expenditures directly related to climate-related activities as part of a registrant's strategy, transition plan and/or targets and goals disclosure requirements under subpart 1500 of Regulation S-K rather than under Article 14 of Regulation S-X.

- Extending a safe harbor from private liability for certain disclosures, other than historical facts, pertaining to a registrant's transition plan, scenario analysis, internal carbon pricing, and targets and goals.

- Adopting a less prescriptive approach to certain of the final rules, including, for example, the climate-related risk disclosure, board oversight disclosure, and risk management disclosure requirements.

- Qualifying the requirements to provide certain climate-related disclosures based on materiality, including, for example, disclosures regarding impacts of climate-related risks, use of scenario analysis, and maintained internal carbon price.

- Removing the requirement to disclose the impact of severe weather events and other natural conditions and transition activities on each line item of a company's consolidated financial statements.

- Eliminating the proposed requirement to disclose any material change to the climate-related disclosures provided in a registration statement or annual report in Form 10-Q.

- Extending certain phase-in periods for the rules.

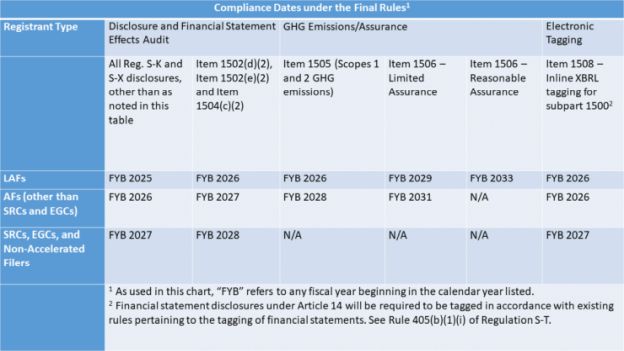

The final rules will become effective 60 days after publication in the Federal Register. The final rules include a phased-in compliance period for all registrants beginning with fiscal years that start in calendar year 2025, with the compliance date dependent on the registrant's filer status and the content of the disclosure as follows:

Stay tuned for a series of in-depth analysis of the final rules in the upcoming weeks, as well as a webinar regarding the same.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.